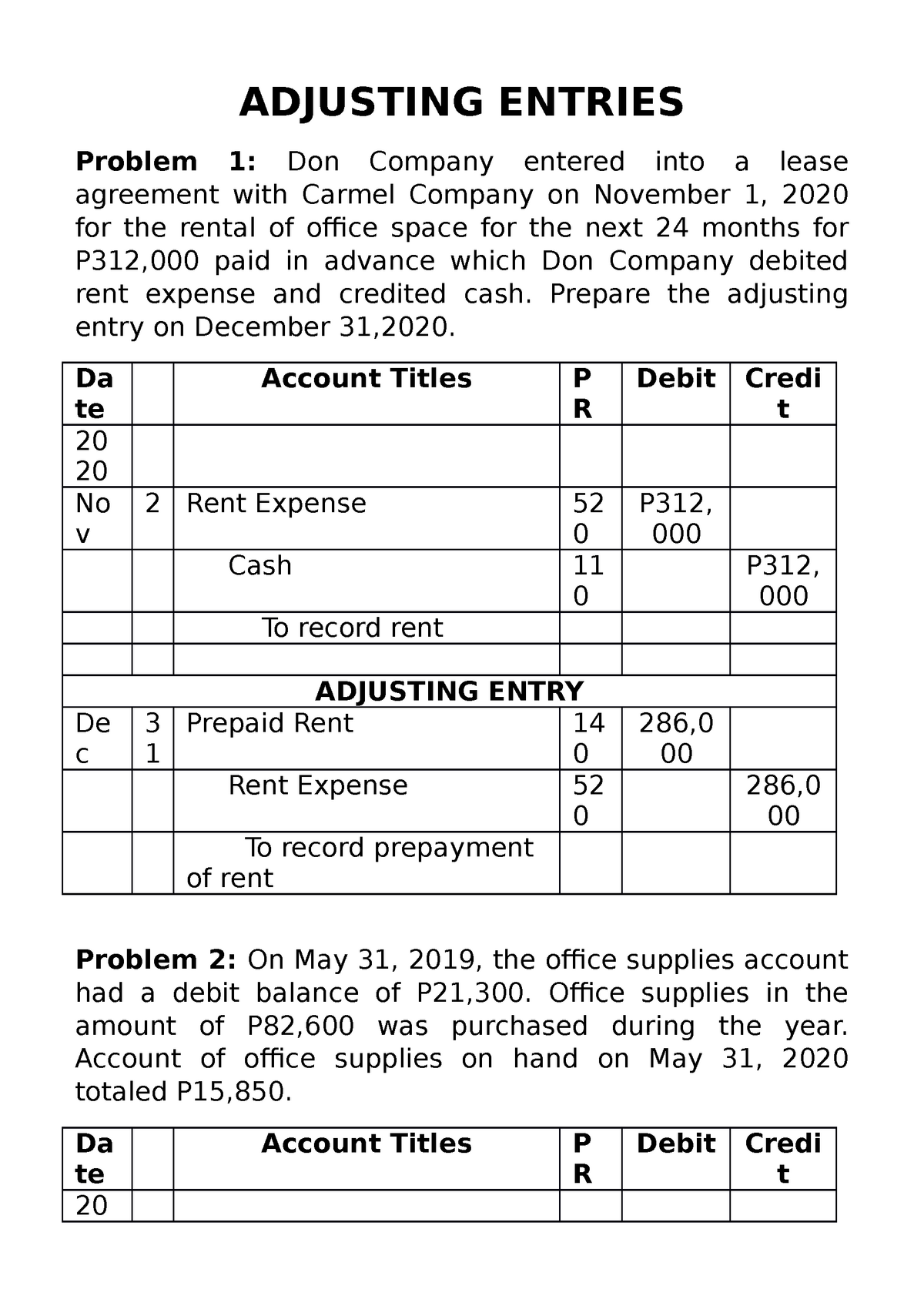

Funky Good fresh fruit Slot Comment: Playtech’s Imaginative Game play

14 de outubro de 2024Better Internet casino Incentives in america Oct 2024

14 de outubro de 2024Katrina Avila Munichiello was an experienced publisher, writer, fact-examiner, and you can proofreader with well over 14 several years of sense working with print and online publications.

What is actually a casing Mortgage?

A casing financial is a type of financing one to funds try the website the brand new strengthening away from a home specifically. The money loaned is usually state-of-the-art incrementally inside strengthening phase once the performs progresses. Generally speaking, the mortgage just requires fee of interest in the construction several months. If building phase is over, the mortgage count arrives due-while some construction mortgages can roll over towards basic mortgage loans.

Secret Takeaways

- A casing mortgage is actually that loan you to pays for building a good new house.

- During design, most financing of this type is actually attract-merely and certainly will disburse money incrementally towards the debtor while the building progresses.

- The 2 preferred particular framework mortgages are stay-alone construction and framework-to-long lasting mortgages.

- The previous are only considering once the a single-year identity, once the latter tend to become a standard financial in the event that home is situated.

- Just like the another type of household endeavor is actually riskier than simply to order a preexisting quarters, framework mortgage loans could be more hard to see and you may hold large cost than just typical mortgage loans.

Just how a houses Mortgage Work

In the event a vintage home loan allows you to buy an existing residence, strengthening on floor up-you start with intense house, that’s-needs a housing mortgage, aka a construction mortgage.

In terms of construction, unforeseen expenses are not arise, increasing the full can cost you. Design mortgages are sought as a way to finest make sure that every-if not completely-strengthening prices are secure punctually, stopping delays regarding end of the property.

As the a different home project try riskier than to get an existing residence, build mortgages could be more difficult to obtain and you may hold high rates than simply typical home mortgages. Still, there are lots of lenders available-one another experts in mortgage brokers and you will antique financial institutions.

Loan providers may offer different options making design mortgage loans more appealing in order to borrowers. This could include interest-just repayments inside the framework stage, and construction-to-long lasting finance, they might also offer locked-when you look at the interest rates when build starts.

Construction-to-Permanent versus. Stand-By yourself Structure Finance

A homes-to-permanent financing try a housing mortgage one to turns to a permanent financial in the event that strengthening is carried out. Commercially, the financing choice keeps two fold: financing to cover the costs out of build and you will a home loan towards the finished home. The main benefit of including agreements is that you have to apply only once, and you may only have you to definitely financing closing.

If your debtor does not sign up for a construction-to-permanent loan, they could utilize a stay-alone design mortgage, and this typically has a single-year limitation label. Instance a houses home loan you will call for a smaller sized down-payment.

The interest rate can not be locked inside the into the a stand-alone build financial. The bottom interest rates can also be more than a property-to-long lasting financing.

The newest borrower may need to apply for another type of home loan to purchase the development financial obligations, which would feel owed once conclusion. This new debtor can sell the established domestic and you can live-in an excellent local rental or other form of homes in build of one’s brand new quarters.

Who does allow them to explore guarantee regarding selling away from the early in the day the place to find safeguards any will cost you after the production of new domestic, meaning the building financial may be the just outstanding personal debt.

Just how to Sign up for a construction Loan

Applying for a construction loan is during certain ways just like trying to get any financial-the procedure boasts a glance at the brand new borrower’s expenses, possessions, and you can income. (Very, expect you’ll give economic comments, taxation statements, W-2s, and you may credit file.) It comes to more.

To help you be eligible for a construction home loan, the newest debtor should have a signed buy or construction price on the creator or creator.

Which contract ought to include of many issues and figures, like the complete endeavor timeline (including the begin and you can expected end dates), and also the total offer amount, that offers for any projected can cost you out of design and you may, in the event the relevant, the cost of the house or property in itself.

Structural illustrations, in depth floor arrangements, and a report on building product-basically, a thorough list that helps take into account the latest finances-are generally area of the bundle.

Your own building builder otherwise structure company will need to give economic statements along with latest licenses and insurance rates papers.

At a minimum, most lenders want a beneficial 20% down-payment for a construction home loan (some require to 31%). That is not so different than the prerequisites for almost all conventional mortgage loans.

But with your creditworthiness, lenders usually are shopping for their exchangeability. They might expect a lot of dollars booked inside the situation building can cost you getting greater than questioned. So if you’re going for a stay-alone construction loan, understand that its very small-term-and when the brand new year’s right up, your most useful be happy to pay back or in a posture so you can qualify for the newest money.

What exactly is a property Mortgage?

A homes mortgage, otherwise build home loan, are a preliminary-term financing you to a creator otherwise homebuyer removes to finance the creation of another type of house. Rather than a lump sum payment, this new money try delivered during the mentioned durations, made to shelter the actual design months. Normally long-term no further than just one year, some structure funds instantly become permanent mortgages in the event that strengthening is finished; someone else simply cancel, requiring refinancing to be an everyday mortgage.

Just what are Structure Financing Rates?

Structure financing interest levels fluctuate, always combined with prime interest rates-whether or not which includes funds, the interest rate would be secured set for a particular months. Even so, overall, he’s normally more than antique mortgage loan loan rates just like the framework funds are thought riskier:

There’s no established home to utilize given that security but if the fresh borrower non-payments. Interest selections have a tendency to differ centered on if you may have a good stand-alone build financing or a housing-to-long lasting loan; full, these money work on at the least step 1%-and often cuatro.5% in order to 5%-more than typical home loan pricing.

Could it possibly be More difficult to locate a construction Financing?

Yes, its much harder to track down a construction mortgage than simply a normal financial. Not only do new debtor need certainly to bring monetary guidance, although builder or builder really does also. They have to submit a signed design deal plus an in depth project routine, a realistic budget, and you may a thorough listing of framework facts. Certain loan providers lay a lot more stringent creditworthiness standards getting framework finance and request higher down costs also.

The conclusion

If you’re looking to build a house about floor right up instead of purchasing one already made, you want a casing loan to finance our home. Money are often put out during the installments once the construction motions out-of that phase to another location. Abreast of conclusion of the property, your loan are able to turn into the a basic financial.